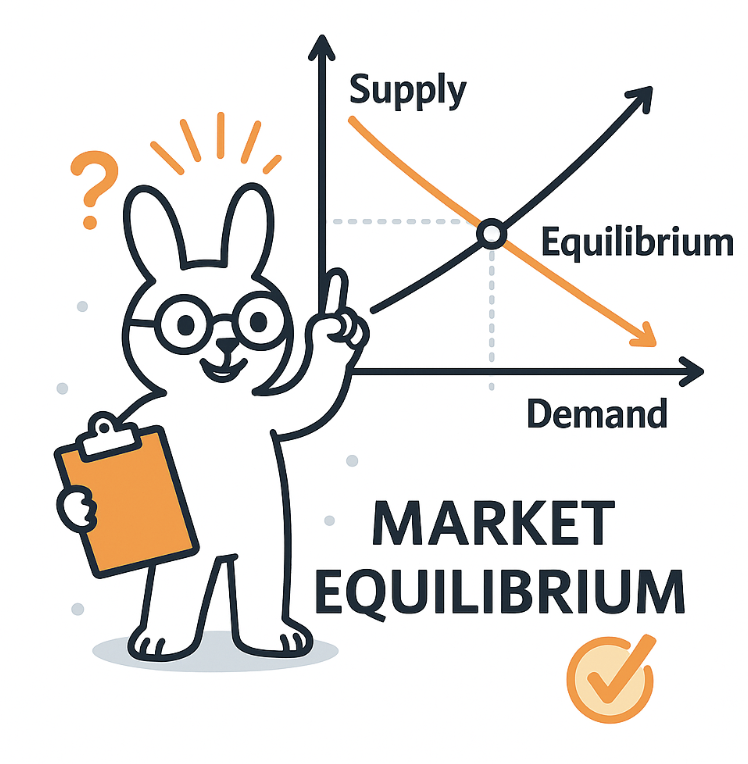

How perfect competition works

In a perfectly competitive market, no single firm can raise its price because buyers can instantly switch to identical products from other sellers. The market sets one price for everyone, and each firm decides how much to produce by comparing that price to its costs.

If the market price is higher than the firm’s marginal cost, the firm produces more; if it’s lower, the firm produces less. Over time, new firms enter when profits are high and leave when profits fall, pushing the market toward a long-run equilibrium where firms earn exactly normal profit - no more, no less.